WHAT HAPPENS AFTER FILING CHAPTER 7 BANKRUPTCY

Bankruptcy can be a sound solution for people with unsettled debt. It can also support them to persevere onto significant assets, restore their credit, and ascertain a constant financial route forward. Nevertheless, bankruptcy has constraints that you necessitate to know if you’re exploring debt relief.

Remember there are several variables depending on the kind of bankruptcy you explore and the kind of debt you’re suffering. If you have questions about your problematic debt, speak with a Bankruptcy attorney in Staten Island NY, and understand the limitations that you need to know if you’re seeking debt relief.

WHAT HAPPENS AFTER FILING CHAPTER 7 BANKRUPTCY

While considering your debt-relief alternatives, you may wonder what happens after you file for bankruptcy. Bankruptcy is a legitimate process that sets off a chain response of events. Some of these events are to defend you while others are to defend creditors.

1. Appointment of a Bankruptcy Trustee

A bankruptcy trustee will be appointed to supervise your filing. The bankruptcy trustee determines your wealth, will review your paperwork, and either leads at and/or potentially pose inquiries at the conference of creditors.

2. Automatic Stay Goes into Effect

Probably the best thing that follows after filing for Chapter 7 bankruptcy is that an automatic stay goes into effect. This stay prevents creditors from seeking further action to accumulate against you, including:

- Starting or proceeding with legal procedures against you

- Making, culminating, or implementing a lien against your property

- Reaching you by telephone or mail

- Foreclosing your home

- Repossessing your property

- Garnishing your wages

- Demanding your financial balances

3. The Creditor Meeting Is Scheduled

The creditor conference is a hearing that your assigned bankruptcy trustee handles where he asks questions about your assets, financial conditions, and bankruptcy filing work. It is usually the only time you have a conference. This is not a court and no judge is present in the meeting. Your bankruptcy lawyer accompanies the meeting with you. Creditors have the right to attend the conference, but they normally don’t.

4. You’ll Get Reaffirmation Agreements

You might get reaffirmation agreements from creditors requesting you to reaffirm the debt so that it is not discharged during the bankruptcy process. If you are hoping to keep your home or car that is currently burdened, your bankruptcy lawyer may advise consenting to these agreements.

5. Personal Financial Management Course

You will be needed to finish a personal financial management course before you obtain your discharge. This course is an extension of the credit counseling you received prior to filing your petition.

6. You Receive Your Discharge

At last, you will get your discharge. Your discharge gives you a new beginning and eliminates the legal obligation for you to return any of the settled debt.

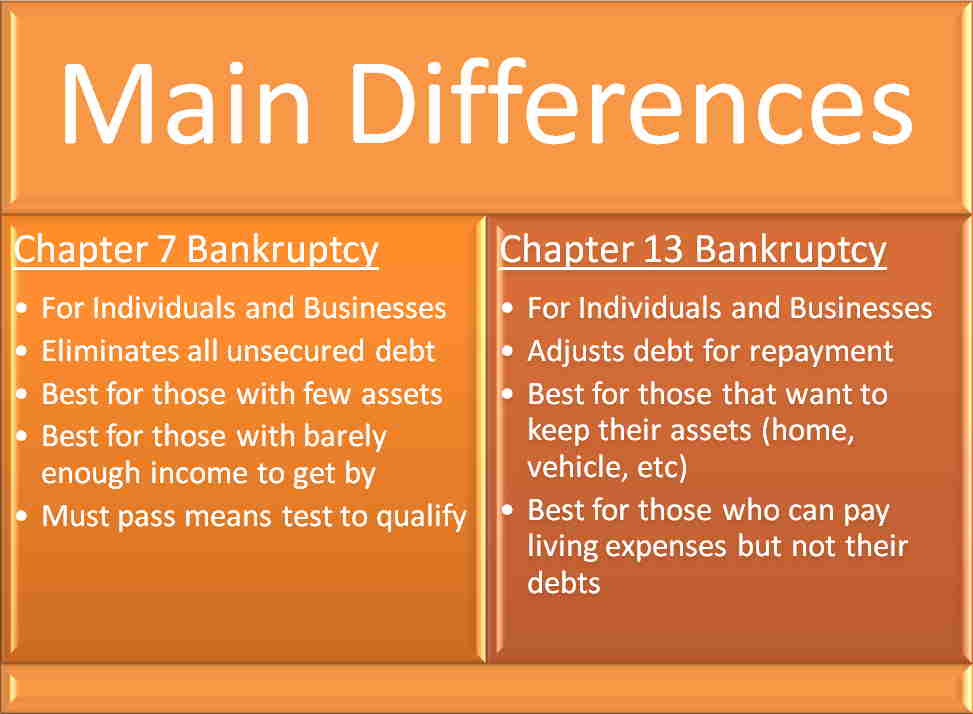

Chapter 7 Bankruptcy vs Chapter 13 Bankruptcy

Does chapter 7 bankruptcy clear all debt?

No. Few debts cannot be discharged in chapter 7, including:

- Alimony

- Many types of non-support marital obligation

- Child support

- Criminal compensation

- Most study loans

- Court fines

- Some duty obligations

- Debt caused by misrepresentation, defalcation of trustee debt and pernicious injury